When you think of the Federal Government, like most people, you probably imagine there isn’t much you can do to speed it along or give it a push. Normally, you might be okay with that, but now, you’ve applied for your Employee Retention Tax Credit.

Waiting around for the IRS to review, process, and deliver the expected credit can be a frustratingly slow process and is just another thing for business owners to worry about. You might be like many business owners who are looking to receive their ERC payout as soon as possible — which is why you’re here.

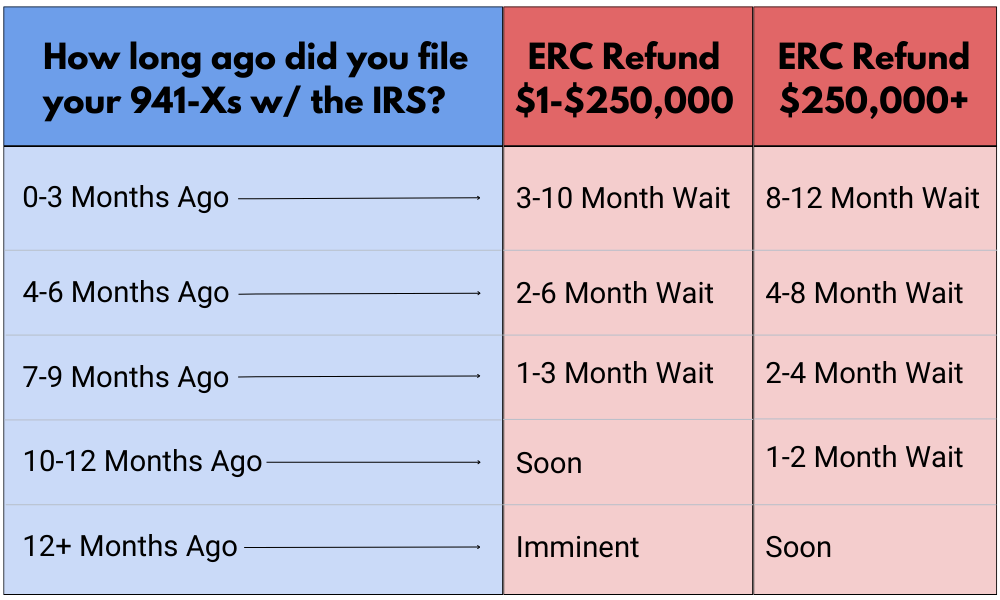

In a hurry? Check your approximate ERC refund status quickly:

With rising inflation, uncertainty in the economy, and a business to run — receiving your employee retention credit sooner could be an absolute game-changer in 2024.

If this sounds like you and are wondering if you can get your ERC loan faster. Fortunately, there is a way: ERC Advance Payments.

And to make that process even easier, you can work with an Employment Retention Credit Loan Provider.

“Your organization could be eligible for up to $26,000 per employee in employee retention tax credit (ERTC) even if you have already received PPP loans.” — ERC Assistant

In this article, you’ll learn everything you need to know about ERC advance payment, including how to receive it, how to apply for it, and many other answers to the most frequently asked ERC questions.

So without further ado, let’s get right into the nitty gritty of ERC advance payments!

Employee Retention Tax Credit: At A Glance

In case you do not know exactly what the Employee Retention Tax Credit is, it is a refundable tax credit passed through the CARES Act for eligible employers that retained their employees during the COVID-19 pandemic.

The credit is available to employers who experienced a full or partial shutdown of their operations due to COVID-19, as well as those who experienced a significant decline in gross receipts. To be eligible, employers must have been in operation since at least March 12, 2020, and must have retained their employees throughout the shutdown.

Employers can claim the credit for each calendar quarter beginning after March 12, 2020, and ending before December 31, 2021.

The credit is equal to 50% of the qualified wages paid to eligible full-time and full-time equivalent employees during 2020, (up to $10,000 per employee per quarter), and 70% for 2021, meaning an employer can claim a total credit of $26,000 for the year 2021). For employers with more than 500 employees, the total credit is capped at $5 million.

An Employee Retention Credit Loan Provider (ERCLP) is a type of financial institution that provides loans to businesses who qualified and submitted their claim to the ERTC. These loans are typically used to cover a myriad of business expenses including the costs of salary and benefits, associated expenses such as training and development, and any other aspect of the company that could use the cash infusion. In short, these loans provide valuable cash for your business to use it for what ever reason and best position your company to weather a tougher economic climate.

Benefits of working with an Employee Retention Credit Loan Provider:

✅ Access full loan amounts upfront

✅ Create more operational cash flow

✅ Benefit from tax-deductible interest

How can I get my ERC Loan faster?

To receive an advanced payment, you will need to see if you qualify for an ERTC loan. Many companies and business owners across the country would rather see the cash now rather than wait nine to twelve months from now when they receive their ERTC payout from the IRS.

Of course, most ERC loans will require you to give up something in return, which normally means a small percentage of your ERTC payment. However, if you need these pandemic-related funds sooner rather than later, this may be your best option.

Why are business owners applying for advanced payments of their ERTC reward?

1) IRS Backlogs

Initially, the employee retention tax credit was designed for the United States government to reward companies who retained employees despite COVID-19 related shutdowns and losses.

However, with the rise of ERTC applications and the limited workforce available to review these applications, the reward period has ballooned from three to six weeks to some ERC claims taking six months to a year to resolve.

2) Lack of communication

After applying for this employee tax credit, many business owners have been waiting. And waiting… and waiting. With no ability to speed the process up, many have tried contacting the IRS to check on the status of their claim.

While calling the IRS helpline may provide you with information on your application, it will not speed up the review process. Luckily, an employee retention credit loan provider can evaluate your claim and reward you a lump sum much sooner than the IRS.

How To Receive an ERC Advance Payment

The ERC Advance Payment process can vary depending on the ERTC loan service you are working with.

However, it generally involves several of the following steps:

1) Provide the loan provider with your business details to help them understand your employee retention credit claim

2) Complete your online application and submit your qualifying documentation

3) Connect with a funding specialist who will provide a consultation

4) Receive the approval decision

Tip! Getting your ERC Advance Payment early allows you to enjoy flexibility with interest-only payments, access dedicated funding specialists whose sole purpose is to determine what loan best fits your business, and fast funding (sometimes with approvals as quick as 24 hours and funding within 72 hours).

ERC Advanced Payments – Important Questions (FAQ)

Is an ERTC loan right for my business?

As long as you meet the qualifications for the Employee Retention Tax Credit, you should be eligible to apply for an ERTC loan. Since your reward from the IRS will eventually be processed, you can receive a good chunk of that money sooner while paying interest on the loan once your claim has been rewarded.

For more information about receiving an advanced payment on your ERTC, work with a dedicated financing group that will review your application and determine your best course of action.

What documents do I need for an ERTC advance payment?

To receive ERTC advance payment, you will need to be able to demonstrate that your business was negatively impacted by the pandemic with supporting payroll, government orders, and gross receipts, and provide Form 941 and Form 941-X for all quarters included in your ERTC filing. You will also need to show proof of submission to the IRS through a FedEx or UPS tracking number. This is the complete list of documents needed for an ERTC advance payment:

- IRS 941’s for 2019, 2020, and 2021 (whichever is relevant)

- Signed IRS 941x’s for 2019, 2020, and 2021 and proof of submission to IRS

- Payroll Documents by pay period from March 1, 2020 through Sept 30, 2021

- ERC calculation & explanation (eligibility/impact statement)

- If applicable: PPP Forgiveness Application Draw 1 Form 3508

- If applicable: PPP Forgiveness Application Draw 2 Form 3508

Luckily, you can prequalify here to determine your eligibility and begin submitting the necessary paperwork with a trusted ERTC loan provider to get the process started.

What is the shortest amount of time I could receive my money for an ERTC loan?

The average time to complete the ERTC loan process and receive your money is typically between 2-3 weeks. You can expedite this by having all the necessary documents submitted within the first 48 hours to receive your money in as little as 7 days and with same day wiring, you will able to access the loan funds in a matter of hours.

Does the ERTC loan for advance payment affect my credit score?

No, the ERTC loan does not have any impact on your credit score. The loan application and review does not include a FICO check. Also, these is no need for the ERTC loan providers to request a soft or hard credit pull so the credit score will remain unchanged.

Can I receive advance payments for the employee retention credit?

Employers can receive advance payments of the Employee Retention Credit by applying for an advance payment from a dedicated ERTC loan provider.

Originally, business owners could complete Form 7200 and submit it to the IRS. However, this form is no longer available which means that an ERTC loan is most likely your best bet to receive a reward payout in the next few weeks.

How do ERTC loans and financing approvals work?

Employee Retention Credit refunds have a turnaround time ranging from 9-12 months, but by taking out a loan on your expected tax credit — typically with interest rates ranging from 10% to 30% — funds can be deposited in 2-4 weeks.

This can be especially useful if you are needing to quickly shore up capital during trying times. Additionally, an ERTC loan can potentially have a higher likelihood of approval than other types of business loans due to the fact that your business prequalifies for a government reward.

How is the ERC loan paid out?

A Employee Retention Tax Credit loan is usually given out after a full review of your company, your ERTC application, and other contributing factors to determine the size of your expected ERTC reward. Since you will be receiving this reward as a loan, the provider will set an interest rate along with additional application fees.

These vary from company to company, so it is important to see which kinds of fees your loan provider is charging.

The trade-off is waiting around a month or less instead of the standard 9 months to a year. The funds can be deposited directly into the appropriate account.

Can you be paid upfront for the ERC lending program?

Yes, you can be paid upfront for the Employee Retention Tax Credit and the process has proven to be fairly easy. You just need to provide the names and dates of birth of the majority owners, the ERC calculations used to determine the anticipated credit, and the appropriate documentation, including the aforementioned 941-Xs and supporting payroll, government orders, and gross receipts.

What are the ERC loan requirements?

Perhaps most significantly, the owner and borrower have to be credible. To be deemed credible, the business owner in question must be in good standing with creditors, cannot have bankruptcies, or have committed any recent felonies. However, there are no cash flow requirements or minimum credit scores.

Are there companies that offer ERC loan financing?

Yes, there are companies that offer ERC financing. These companies provide loans or lines of credit that can be used to cover the cost of the credit, allowing businesses to take advantage of the credit without any out-of-pocket costs.

In addition, many of these companies offer flexible repayment options, making it easy for businesses to repay the loan over time. ERC financing companies and other ERC service providers can help you to also avoid falling into ERC scams.

How do I apply for an ERC loan Advance?

Applying for an ERC advance is not all that different from the process of applying for the Employee Retention Credit through an Employee Retention Credit company.

Most ERC loan companies that are able to facilitate an ERC advance are going to need you to create a profile with basic business information. After making a profile, complete an online application and submit the qualifying documentation.

This is the step during which you will also provide your Form 941 and Form 941-X for all quarters included in your ERTC filing. One of the final steps is connecting with an ERTC funding specialist that will match you with the ideal funding option for your business. After that, you will typically receive a funding decision in a few days.